Recycling Industry Tax Compliance Report (2023)

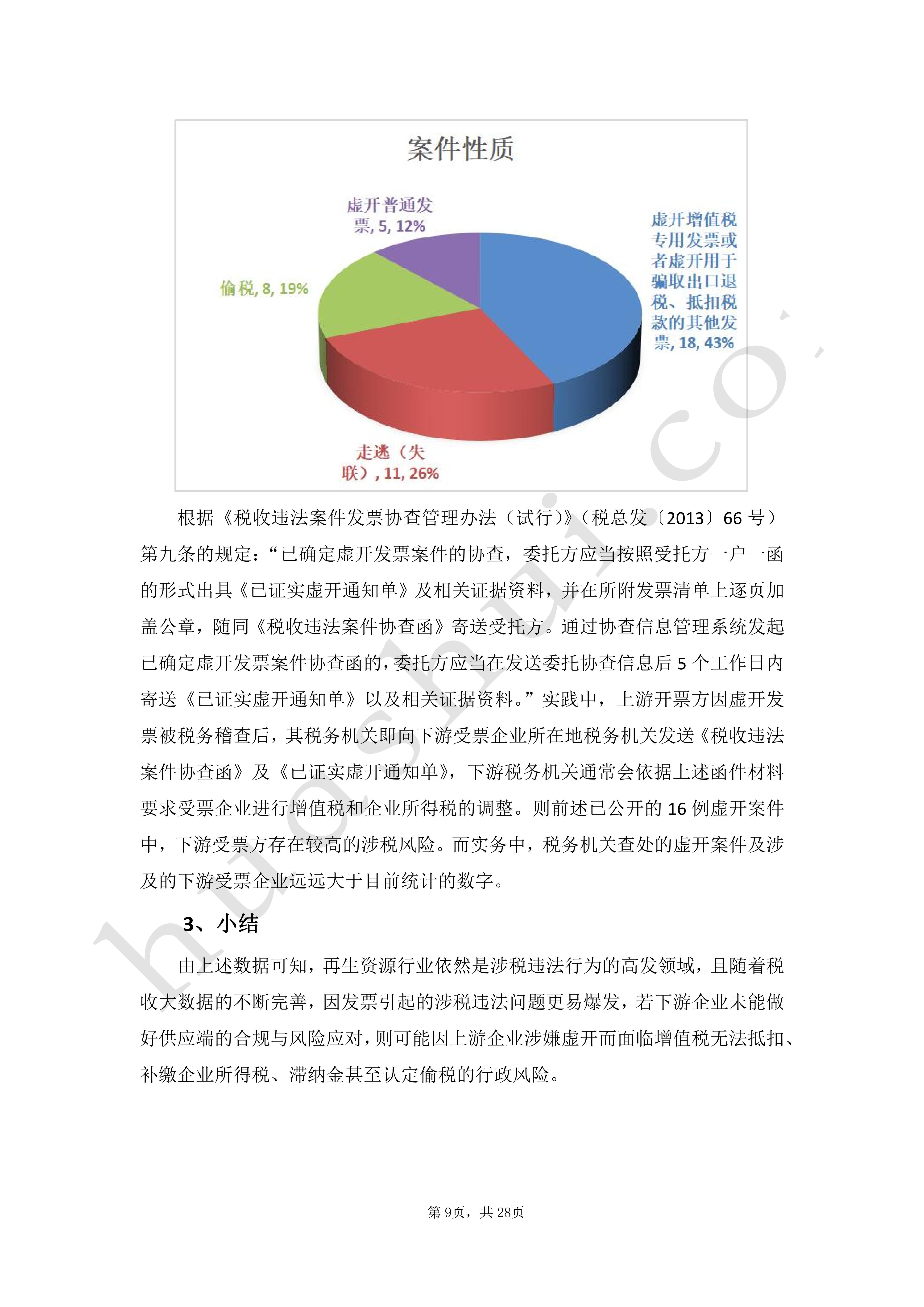

For a long time, due to the special nature of the recycling business of the renewable resources industry, the VAT input of the procurement process of renewable resources enterprises has been seriously insufficient, and in order to make up for the shortfall in input, some enterprises have obtained VAT invoices by changing their business model, third-party issuance or even purchase. As the special action of "Fighting Frauds and Crooks" has gradually deepened and turned into a regularized crackdown, a large number of cases of false VAT invoices have broken out in the renewable resources industry, and most of the enterprises and their persons-in-charge have been involved in administrative or even criminal liabilities. Under such circumstances, many enterprises have no choice but to give up obtaining input invoices and choose to use homemade vouchers for pre-tax deduction of enterprise income tax, while at the level of value-added tax (VAT), they pay VAT in full according to the sales amount when selling goods to the downstream, which greatly compresses the profit margins of enterprises.2021 On December 30, 2012, the Ministry of Finance (MOF) and the State Administration of Taxation (SAT) jointly issued the Announcement of the Policy of Improving the Value-added Tax for Comprehensive Utilization of Resources (Announcement of MOF and SAT). On December 30, 2021, the Ministry of Finance and the State Administration of Taxation jointly issued the Announcement on Improving VAT Policies for Comprehensive Utilization of Resources (Ministry of Finance and the State Administration of Taxation Announcement No. 40 of 2021), in which the provisions on the sales of renewable resources by general taxpayers can choose the simplified tax method to calculate and pay the VAT according to the 3% levy rate have greatly alleviated the problem of VAT burden in the recycling business. At the same time, in the process of handling criminal cases of false invoicing of renewable resources enterprises in the past two years, practical cases of the crime of illegal purchase of VAT invoices have appeared, and at the same time, with the reform of criminal compliance mechanism of the procuratorate system being comprehensively pushed forward in the country, the compliance of non-prosecution is also fairly utilized in the tax-related criminal cases of the renewable resources industry, and the above changes have brought a new opportunity for the defense of the tax-related criminal cases of the renewable resources industry. The above changes have brought new opportunities for the defense of tax-related criminal cases in the renewable resources industry. Based on this, in order to enable the majority of enterprises in the renewable resources industry to carry out tax management in compliance and legally, strengthen internal risk prevention and control and external risk isolation, and effectively cope with and resolve tax-related legal risks in their future operation, Huatax has combined the continuous research of the renewable resources industry and the experience of representing the latest tax-related cases to prepare this report, which provides information on the tax environment of the renewable resources industry under the new situation of tax levy and administration, causes of the tax risks, the main tax risks and their manifestations, the tax risks and the forms of fraudulent prosecution, the tax-related criminal cases, and the tax-related criminal cases in the renewable resources industry. This report provides in-depth analysis on the tax environment of renewable resources industry under the new situation of tax administration, causes of tax-related risks, major tax-related risks and their manifestations, points of contention and defense in criminal cases of fraudulent invoicing, and tax compliance management, etc., with a view to providing useful references and reference for the enterprises of renewable resources industry.

Click to download: Full Text of Recycling Industry Tax Compliance Report (2023)