Unreported Investment Recovery Leading to Tax Supplementary Payment: Compliant Application of Overseas Investors’ Reinvestment Incentives

Editor’s Note: According to data from the Ministry of Commerce, more than 70,000 new foreign-invested enterprises were established in China in 2025, representing a year-on-year increase of 19.1%. The continuous increase in foreign investment in China is largely attributable to supportive tax policies. Since 2017, China has established a deferred tax regime for overseas investors making direct investments with distributed profits. *The Notice on Expanding the Scope of the Policy of Temporary Exemption from Withholding Income Tax on Direct Reinvestment by Overseas Investors with Distributed Profits* (Cai Shui [2018] No. 102) extended the application of tax deferral from encouraged foreign investment projects to all non-prohibited foreign investment projects and sectors. *The Announcement on Tax Credit Policies for Direct Reinvestment by Overseas Investors Using Distributed Profits* (Announcement No. 2 of 2025 jointly issued by the Ministry of Finance, the State Taxation Administration and the Ministry of Commerce), released last year, further added tax credit incentives on the basis of the deferred tax system. This marks a leap forward in tax policies for foreign investors' reinvestment, evolving from "tax deferral" to "tax reduction", which is of great significance for easing the burden on foreign investors, improving operational quality and efficiency, and boosting their investment enthusiasm. Based on two cases of supplementary tax payment arising from overseas investors' reinvestment, this paper explores the core application requirements of the deferred tax policy, interprets the key points of the new tax credit policy, and provides practical references for overseas investors to enjoy tax incentives in a compliant manner.

I. Case Study: Failure to Timely Report and Pay Taxes on Investment Recovery Leads to Risk of Supplementary Tax Payment

Case 1:

Company J is a wholly-owned subsidiary of Company H based in Hong Kong, China. In May 2019, Company J distributed dividends and bonuses totaling 72 million yuan to Company H. Company H directly reinvested the received dividends and bonuses in China to establish a new Company M engaged in marketing activities. Company H met the eligibility criteria for the deferred tax policy and deferred the payment of 7.2 million yuan in withholding income tax in accordance with the provisions. In May 2020, the competent tax authority of Company J found that the shareholders of Company J had changed from Company H to three individuals including Person A, all of whom were senior executives of Company J; the shareholder of Company M remained unchanged, still being Company H. Further verification showed that the relevant parties had completed the tax formalities and paid the income tax in connection with this equity transfer. However, from a business operation perspective, it was unreasonable for Company H to withdraw its investment from Company J, which had relatively stable profits, and invest in a marketing company with no substantive business operations. Therefore, the tax authority set up a special task force and listed Company J, Company H and Company M as key monitoring targets.

In January 2021, the special task force learned through a third-party platform that Company H was in liquidation. Generally, a company will settle its assets and liabilities before deregistration and liquidation. For its subsidiary Company M, Company H may have recovered its registered capital by directly withdrawing the investment or transferring equity. The task force initiated a tax information exchange with the Inland Revenue Department of Hong Kong, China. According to the reply from the Inland Revenue Department of Hong Kong, China, Company H had been deregistered and dissolved on January 3, 2021. The entity eligible for the deferred tax policy had been dissolved, yet the investee Company M continued to operate normally with no change in its registered capital. This indicated that Company H might have transferred its equity in Company M prior to its dissolution. Based on this, members of the special task force communicated with the person-in-charge and financial personnel of Company M again, and finally confirmed that Person A and other individuals, the former legal representative of Company H and senior executives of Company J, had succeeded to the equity in Company M held by Company H. In other words, Company H had recovered the investment eligible for the deferred tax policy and was required to file and pay the deferred taxes in accordance with the provisions of Cai Shui [2018] No. 102. With the policy guidance from the special task force, Company M took an active cooperative attitude, contacted the original investors and relevant personnel in Hong Kong, China, and finally paid a total of 7.99 million yuan in supplementary taxes and late payment surcharges.

Case 2:

An article published in *China Tax News* in January 2026 indicated that Company H is a wholly-owned subsidiary of an overseas enterprise Company Z. In 2018, Company H distributed 900 million yuan in profits to its parent company Company Z, which then directly reinvested the profits in another wholly-owned subsidiary Company A in China and enjoyed the deferred tax incentives. Recently, tax officials learned that Company Z planned to reduce the registered capital of the investee Company A by 1.5 billion yuan in the near future. To verify the authenticity of the capital reduction plan and accurately confirm the exact time of the capital reduction by the overseas Company Z, tax officials used big data platforms and internal and external information tools such as Tianyancha to monitor and verify the shareholder information and equity change of Company A, focusing on tracking and verifying the changes in Company A's registered capital and Company Z's investment ratio in Company A, so as to obtain information such as the time and amount involved in the capital reduction; they also strengthened communication and cooperation with the competent tax authority where Company A is located, requesting it to assist in verifying the dynamic situation such as whether the enterprise has reduced its registered capital.

After implementing a series of verification measures, tax officials confirmed the fact of Company Z's capital reduction, which involved 900 million yuan that had enjoyed the temporary tax exemption policy. The deferred taxes should be paid in accordance with the tax laws. Through pre-policy guidance and dynamic monitoring, tax officials successfully helped Company Z mitigate the risk of underpayment of taxes arising from the recovery of its investment, enabling it to file and pay 45 million yuan in taxes in a timely manner.

II. Accurately Grasp the Conditions for Deferred Taxation and Pay Attention to Tax Obligations Upon Investment Recovery

According to the provisions of the *Enterprise Income Tax Law*, China has the taxing right over the income derived by non-resident enterprises from sources within China. To encourage long-term foreign investment in China, Cai Shui [2018] No. 102 stipulates that where overseas investors directly reinvest their domestic profits in China and meet the prescribed conditions, the enterprise income tax on such profits may be temporarily exempted from withholding. The deferred taxes shall be declared and paid only after the overseas investors actually recover the direct investment that has enjoyed the temporary exemption from withholding income tax through equity transfer, share repurchase, liquidation and other means. This policy plays an important role in easing the capital pressure on foreign investors, improving operational quality and efficiency, and boosting their investment enthusiasm.

According to the provisions of Cai Shui [2018] No. 102 and *Announcement on Issues Concerning the Expansion of the Scope of Application of the Policy of Temporary Exemption from Withholding Income Tax on Direct Reinvestment by Overseas Investors Using Distributed Profits* (Announcement No. 53 of 2018 of the State Taxation Administration), overseas investors must meet the following three conditions simultaneously to enjoy the deferred taxation on profit reinvestment: First, the investment method must be direct investment, including equity investment activities such as capital increase, new establishment and equity acquisition with distributed profits; the supplementary payment of the subscribed registered capital also falls within the scope of compliant direct investment. Second, the profits must be derived from equity investment income such as dividends and bonuses distributed by the profit-distributing enterprise. Third, in terms of capital flow, the funds (assets) used for investment must be directly transferred from the profit-distributing enterprise to the investee enterprise or the equity transferor, and indirect transfer is not allowed.

In the specific application of the deferred tax policy, both overseas investors and profit-distributing enterprises shall pay attention to the declaration requirements: For overseas investors, they shall fill in the *Information Report Form for Deferred Payment of Withholding Income Tax by Non-Resident Enterprises* and submit it to the profit-distributing enterprise; the profit-distributing enterprise shall examine the materials and information submitted by the overseas investor, confirm that the information filled in by the overseas investor is complete with no missing items, and that the actual profit payment process is consistent with the information filled in by the overseas investor. Within 7 days from the date of the actual payment of profits, the profit-distributing enterprise shall submit the *Enterprise Income Tax Withholding Declaration Form* and the *Information Report Form for Deferred Payment of Withholding Income Tax by Non-Resident Enterprises* (supplemented with information by the profit-distributing enterprise on the basis of the submission by the overseas investor) to the competent tax authority. If an overseas investor actually recovers the direct investment that has enjoyed the temporary exemption from withholding income tax policy, it shall, within 7 days from the date of actual receipt of the corresponding funds, declare and pay the deferred taxes to the tax authority in accordance with the prescribed procedures.

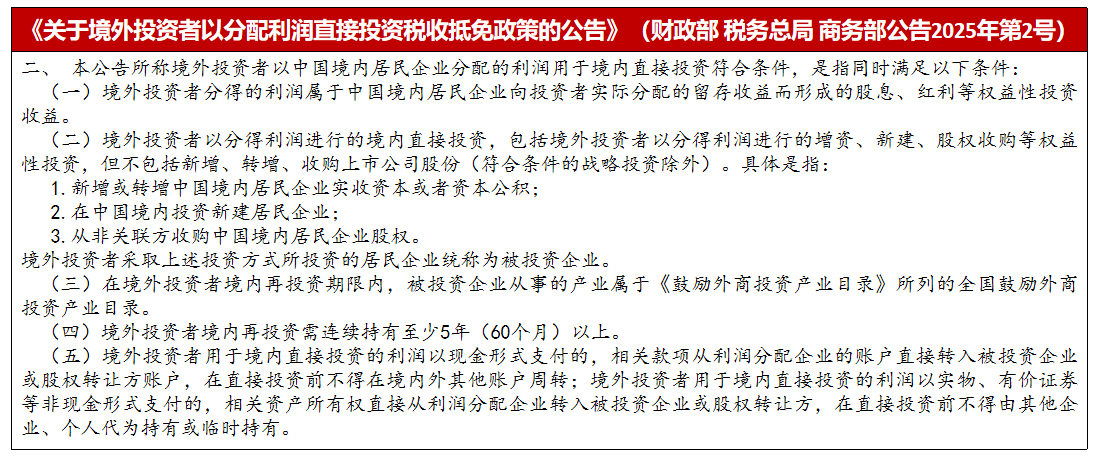

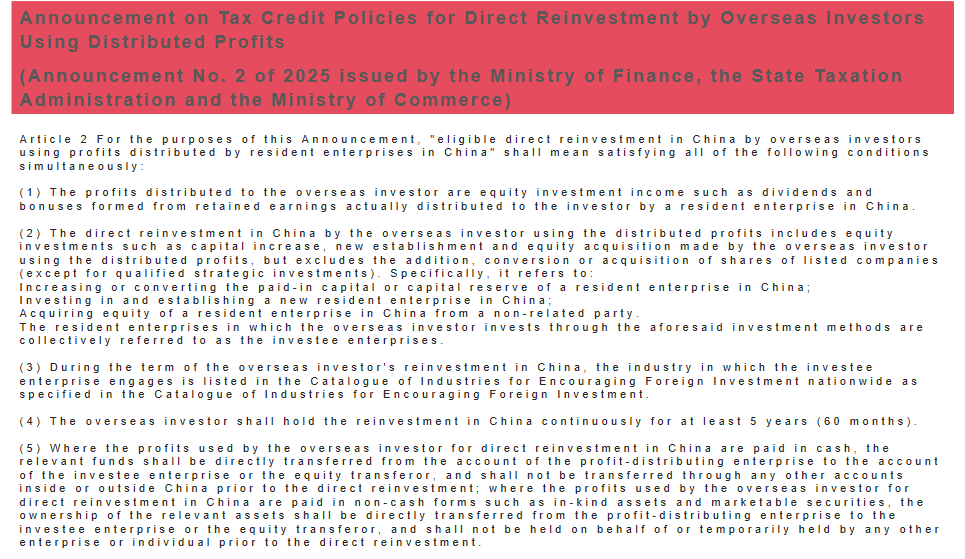

III. Policy Upgrade: Eligible Domestic Reinvestment by Overseas Investors Entitles to Tax Credits

In June 2025, the Ministry of Finance, the State Taxation Administration and the Ministry of Commerce jointly issued *Announcement on Tax Credit Policies for Direct Reinvestment by Overseas Investors Using Distributed Profits* (Announcement No. 2 of 2025 of the Ministry of Finance, the State Taxation Administration and the Ministry of Commerce), clarifying that overseas investors who make eligible direct reinvestment may enjoy a tax credit incentive equivalent to 10% of the investment amount. In July, the State Taxation Administration issued *Announcement on Matters Concerning the Tax Credit Policy for Direct Reinvestment by Overseas Investors Using Distributed Profits* (Announcement No. 18 of 2025 of the State Taxation Administration), which specified the relevant tax collection and administration measures. Under this policy, the tax incentives for overseas investors' reinvestment are more significant. For example, in October 2025, overseas investor Company X received 10 million yuan in profits distributed by domestic Company Y, and used the entire amount to increase the capital of Company Y, meeting the eligibility criteria for the tax credit policy. Assuming that the overseas investor selects a 10% tax credit ratio, a tax credit quota of 1 million yuan will be formed. On July 1, 2026, Company Y paid 6 million yuan in royalties to Company X, which may declare a deduction of 600,000 yuan in taxes against the tax credit quota.

According to the provisions of Announcement No. 2 of 2025, the relevant conditions include that the industry engaged in by the investee enterprise is listed in the *Catalogue of Industries for Encouraging Foreign Investment*, and that the overseas investor shall hold the equity from the domestic reinvestment for at least 5 consecutive years (60 months), with the specific provisions as follows:

Enterprises intending to apply for the tax credit incentives should focus on two core points: First, accurately understand and apply the eligibility criteria for the tax credit policy. Compared with the deferred tax policy, the tax credit policy has stricter conditions, including restrictions on the industry of the investee enterprise and the duration of continuous investment. Misapplication of the tax credit incentives may result in the risk of supplementary tax payment. Second, pay close attention to the requirements for material submission and tax declaration. For example, overseas investors shall, through the investee enterprise and via the unified platform of the Ministry of Commerce's business system (the Comprehensive Management Application for Foreign Investment), submit to the local competent commerce department information such as the name and country of the overseas investor, the names and locations of the investee enterprise and the profit-distributing enterprise, as well as the reinvestment time, industry sector and amount, together with relevant supporting documents, and obtain materials such as the *Profit Reinvestment Information Form* after examination and verification.

In addition, for the determination of the applicability of deferred taxation and tax credits, enterprises may seek professional support and apply for an advance tax ruling. For example, the Shanghai Municipal Taxation Bureau recently published a case on the application of the tax credit policy for overseas investors' reinvestment: In April 2025, a German enterprise used a portion of the 2023 profits distributed by its wholly-owned domestic subsidiary Company G to make a direct capital increase of 35.4715 million yuan; Company G is expected to pay 37 million yuan in dividends and bonuses for 2024 to its parent company by the end of 2025, and shall withhold and remit the enterprise income tax in accordance with the provisions. Company G filed an application with the competent tax authority for an advance tax ruling on whether the enterprise income tax to be withheld and remitted on the aforementioned dividends and bonuses is eligible for the tax credit policy for overseas investors' direct reinvestment using distributed profits. Based on the materials and statements provided by Company G, the tax authority held that, on the condition that the German enterprise obtains materials such as the *Profit Reinvestment Information Form* issued by the competent commerce department, the enterprise income tax payable on the 37 million yuan in dividends and bonuses to be received by the German enterprise by the end of 2025 is a taxable amount eligible for credit as stipulated in Article 3 of Announcement No. 2 of 2025. Since the agreed tax rate for dividends under the tax treaty between the Chinese government and the German government is 5%, the enterprise income tax payable by the German enterprise may be offset upon declaration to the competent tax authority when Company G pays the dividends and bonuses to its parent company by the end of 2025, provided that the conditions specified in Article 2 of the Announcement are met. The offset amount is 5% of the capital increase amount, i.e., 1.773575 million yuan. The unused portion of the tax credit in the current year may be carried forward to subsequent years. Based on the above, the tax authority issued an *Advance Tax Ruling Opinion*, confirming that the enterprise is eligible for the tax credit policy for overseas investors' direct reinvestment using distributed profits, which has strengthened the confidence of overseas investors in their continuous investment in China.

IV. Summary

In July 2025, seven ministries and commissions including the National Development and Reform Commission and the Ministry of Finance jointly issued *Notice on Implementing Several Measures to Encourage Domestic Reinvestment by Foreign-Invested Enterprises* (Fa Gai Wai Zi [2025] No. 928), which promotes domestic reinvestment by foreign-invested enterprises through measures such as strengthening project service guarantees, optimizing the allocation of land factors, simplifying and streamlining relevant formalities, implementing and fulfilling supporting policies, and facilitating the use of foreign exchange funds. In the tax field, policies have been further extended from deferred taxation to tax credit incentives, sending a clear signal of China's firm commitment to expanding high-level opening-up. With the extensive application of cross-border tax-related information exchange and tax big data, overseas investors shall accurately interpret the eligibility criteria for relevant policies and apply tax incentives in a lawful and compliant manner.