The financial industry is prone to risks of false opening and tax evasion. How should we effectively respond?

Editor's note: Most of the tax violations in the financial industry are manifested in two types: false invoicing and tax evasion. Through observing these cases, it was found that financial enterprises involved large amounts of false invoicing or tax evasion, involving various financial sub-industries such as trusts, funds, and financing leasing. Based on this, this paper intends to analyze the causes of tax violations in financial enterprises, and propose corresponding strategies for resolving tax administrative and criminal responsibilities.

I. Case observation: Multiple cases reveal tax violations of financial enterprises

Case 1: A trust company was recovered for false invoicing

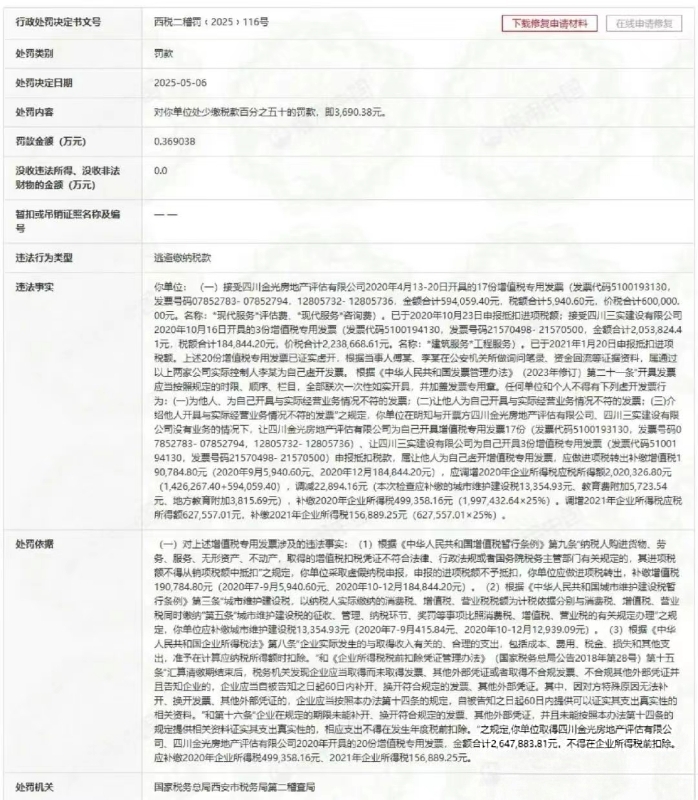

The company involved in the case, Chang'an International Trust Co., Ltd., accepted 17 value-added tax special invoices issued by Sichuan Jinguang Real Estate Appraisal Co., Ltd., with a total value and tax of 600,000 yuan, and declared the input tax deduction amount; Received 3 VAT special invoices issued by Sichuan Sanshi Construction Co., Ltd., with a total value and tax of 2.2386 million yuan, and declared the input tax deduction. The above 20 VAT special invoices have been confirmed to be falsely issued. The tax authorities have based on evidence such as the interrogation records made by the parties Fu and Li at the public security organs, as well as the return of funds, It was determined that the company involved in the case, knowing that there was no real business with Sichuan Jinguang Real Estate Appraisal Co., Ltd. and Sichuan Sanshi Construction Co., Ltd., allowed the issuing party to issue value-added tax special invoices for itself and declare tax deductions, which constituted the act of letting others issue false value-added tax special invoices for themselves. The amount of value-added tax that should be transferred out as input tax is 190,700 yuan, and the amount of corporate income tax paid from 2020 to 2021 is 656,300 yuan.

Case 2: A financial leasing company was transferred to the judicial authorities for falsely issuing more than 100 million yuan in invoices

The Fifth Inspection Bureau of the Shanghai Municipal Taxation Authority of the State Administration of Taxation found that the company involved in the case, Tianyi Financing Leasing (China) Co., Ltd., mainly has the following problems: Issued 150 value-added tax special invoices for others (for oneself), with an amount of 147.6917 million yuan and a tax amount of 25.1076 million yuan. In accordance with the "Tax Collection and Administration Law" and other laws and regulations, the tax authorities will transfer the case to the judicial authorities in accordance with the law.

Case 3: The person in charge of a third-party payment company was sentenced for issuing false invoices of over 1 billion yuan

2017 From 2020 to 2020, the company involved in the case, China Steel Corporation, used its controlled companies A, B, and C, which are agents of prepaid card business, to sell electronic virtual card prepaid cards under the guise of selling electronic virtual card prepaid cards without real transactions. Using China Steel Company, Company A, Company B, and Company C as the invoicing agents, falsely issued value-added tax general invoices to Company G, with a total value and tax of over 1 billion yuan. The sales manager of the business development department of China Steel Corporation was sentenced to three years' imprisonment with a four-year probation as other directly responsible personnel.

Case 4: An investment fund company was punished for failing to declare taxes

The company involved in the case, Wuhu Ruiye Equity Investment Fund (Limited Partnership), transferred wealth management products from 2016 to 2017 without declaring and paying value-added tax, business tax, and additional taxes. No value-added tax and additional taxes were declared and paid for the transfer of shares in 2016. The tax authorities determined that the company involved in the case constituted tax evasion and proposed to impose a fine of 4.61 million yuan, which is 0.6 times the underpayment of taxes.

Summary: The aforementioned cases reflect that the tax violations of financial enterprises mainly focus on false invoicing and tax evasion. The specific analysis of the cases found that the financial enterprises issued false invoices with the characteristics of large amount involved and long duration. Some financial enterprises issued false invoices to deduct taxes and expenses without real business. In addition, tax evasion by financial enterprises has the characteristic of involving a large amount of money, and tax evasion by financial enterprises is manifested in the form of failure to declare income according to regulations.

Ⅱ The analysis of the causes of tax violation in financial enterprises

By analyzing cases of false invoicing and tax evasion by some financial enterprises, in addition to the internal compliance system problems of the enterprises themselves, the differences in the implementation of tax policies by tax authorities for some financial industries may also be the reasons for the tax risks of financial enterprises.

Firstly, the differences in the application of tax calibers in different regions lead to tax risks. As mentioned in the previous case, the fund company involved in the case did not pay relevant taxes and fees such as value-added tax during the transfer of wealth management products and equity, which caused tax risks for financial enterprises. According to the "Notice on the Comprehensive Implementation of the Pilot Program for Replacing Business Tax with Value-added Tax" (Cai Shui [2016] No. 36), "The transfer of financial products refers to the business activity of transferring the ownership of foreign exchange, securities, non-goods futures, and other financial products. The transfer of other financial products includes the transfer of various asset management products such as funds, trusts, and wealth management products, as well as various financial derivatives. "Due to the unclear definition of financial products in tax laws, some local tax authorities have different execution standards, which brings tax risks to the operation of financial enterprises. For example, some local tax authorities believe that only the Shanghai, Shenzhen, and Beijing stock exchanges are publicly traded markets, and the New Third Board belongs to the over-the-counter trading market. Therefore, the stocks of New Third Board companies belong to non-listed company stocks and are temporarily not subject to value-added tax when transferred. Some local tax authorities believe that companies listed on the New Third Board should be subject to value-added tax on the transfer of stocks. In summary, differences in the application of tax standards can also lead to tax risks for financial enterprises. Financial enterprises should pay attention to the application of tax policies for the financial industry in different places.

Secondly, the imperfect internal tax system such as invoice management is also a cause of tax risks. In many cases of tax violations by financial enterprises mentioned above, there is the problem of false invoices issued by financial enterprises, and the false invoices issued by financial enterprises often involve large amounts of money and a large number of false invoices issued. In addition, there are financial enterprises that have not paid relevant taxes as required. This reflects the problems in the tax compliance system of some financial enterprises, such as internal invoice management. There are problems with the invoice management system of financial enterprises, which means that some financial enterprises do not issue invoices or pay taxes in accordance with regulations in their daily operations. They cannot rely on the authenticity of their business and cannot guarantee the consistency of "goods/services, invoices, and funds". This leads to problems in the invoice issued or received by the enterprise and in the payment of taxes, which brings tax risks to the enterprise.

Ⅲ The analysis of the legal responsibility of financial enterprises for falsely opening and tax evasion

Some financial enterprises issue false invoices or evade taxes, which may lead to corresponding administrative or criminal responsibilities. The specific details are as follows:

First, in terms of administrative responsibility. Financial enterprises issue false invoices and evade taxes in violation of the provisions of tax administrative regulations such as the "Invoice Management Measures" and the "Tax Collection and Administration Law". On the one hand, in terms of the administrative responsibilities borne by enterprises, according to Article 21 of the "Invoice Management Measures", the behavior of issuing false invoices mainly includes "issuing invoices for others or for oneself that do not match the actual business situation." Ask others to issue invoices that do not match the actual business situation; Introduce others to issue invoices that do not match the actual business situation. According to Article 35 of the "Invoice Management Measures", the maximum fine for issuing false invoices is 500,000 yuan and the illegal gains are confiscated. According to Article 63 of the "Tax Collection and Administration Law", for tax evasion, a fine of 0.5 to 5 times the amount of tax not paid or underpaid can be imposed, and the unpaid or underpaid tax can be recovered and a late payment penalty will be imposed. For the determination of tax evasion, the tax authorities should determine the behavior based on the subjective purpose of the perpetrator and the tax evasion behavior they have committed. For example, the "Reply of the State Administration of Taxation on Whether the Correction of Declaration and Payment of Taxes during the Tax Inspection Period Affects the Qualification of Tax Evasion Behavior" (Tax General Letter [2013] No. 196) and the Beijing Zhongyou Guomen Oil Material Sales Co., Ltd. and the National Taxation Authority of Shunyi District, Beijing The Administrative Ruling on Review and Trial Supervision (2017) Jingxing Shen 1402 clearly states in the reply that "taxpayers actively make corrections, declares, and pay taxes before the inspection bureau conducts tax inspections, and the tax authorities have no evidence to prove that the taxpayer has subjective intent to evade taxes." "Not treated as tax evasion"; In the judgment, the court also held that "from the circumstances listed in this provision, the subjective aspect of the parties is the necessary constituent element for determining tax evasion." In practice, some enterprises issue false invoices or evade taxes, which do not have corresponding subjective purposes, and the punishment for them does not conform to the principle of consistency between subjective and objective. Therefore, when financial enterprises face tax risks, they can prove that they should not bear administrative responsibility by proving that they do not have the subjective intention of tax evasion or false invoicing.

Secondly, in terms of criminal responsibility. Financial enterprises that issue false invoices and evade taxes may face criminal responsibility for the crime of issuing false VAT special invoices. As for the crime of issuing false VAT special invoices, it requires financial enterprises to have the subjective intent of issuing false invoices to defraud taxes and objectively cause national tax losses. In other words, according to the principle of consistency between subjective and objective, the crime should have both subjective intent and objective results. According to Article 10 of the "Interpretation of the Supreme People's Court and the Supreme People's Procuratorate on Several Issues Concerning the Application of Laws in Handling Criminal Cases of Harmful Tax Collection and Administration," it also emphasizes that the perpetrator must have the intention to defraud taxes and cause losses to the state. Therefore, the perpetrator has no subjective purpose of deceiving the state tax, and objectively does not cause losses to the state tax. Therefore, it should not be deemed that their behavior has the social harm in the sense of establishing the crime of issuing false value-added tax special invoices in the criminal law. Therefore, when financial enterprises face criminal charges related to the crime of issuing false VAT special invoices, they can combine the facts of the case to resolve their criminal responsibility from both subjective and objective aspects.

IV. Concluding The frequent occurrence of false and tax evasion risks in financial enterprises is related to the identification and application of tax preferential policies and the management of invoices by financial enterprises. For financial enterprises, establishing a sound tax compliance system, correctly applying tax preferential policies, and strictly managing invoices can help enterprises avoid tax risks. If a financial enterprise is liable for administrative or criminal liability due to tax risks, it can demonstrate from both the facts and legal provisions that its behavior does not constitute false invoicing or tax evasion. When unable to cope with tax risks, financial enterprises can rely on the power of professionals to effectively respond to tax administrative or criminal responsibilities, avoid the expansion of risks, and avoid bringing more serious legal responsibilities to the enterprise.