What will be the impact of the judicial interpretation of the Supreme People's Court and the Supreme People's Procuratorate on the convicted cases of false VAT invoices in the petrochemical industry?

Editor's Note: The Interpretation of the Supreme People's Court and the Supreme People's Procuratorate on Several Issues Concerning the Application of Law to the Handling of Criminal Cases of Endangering the Administration of Tax Levies (Legal Interpretation [2024] No. 4) makes it clear that false invoicing that does not aim at fraudulently offsetting the taxes and does not result in a fraudulently lost tax due to the offsetting does not constitute the offence of falsely invoicing for value-added tax. Accordingly, it can be seen that the legal interests protected by the offence of false invoicing of VAT specifically refers to the VAT collected and managed by way of credit, and this conclusion is not created by the judicial interpretation of the Supreme People's Court and the Supreme People's Procuratorate, but is the original meaning of the criminal law, which is also applicable before the implementation of the judicial interpretation of the Supreme People's Court and the Supreme People's Procuratorate. Tax-related cases in the petrochemical industry mainly infringed upon the interests of consumption tax, and the perpetrators usually did not have the purpose of fraudulently offsetting VAT, nor did they have the possibility of causing VAT losses. However, in the past, in the trial of petrochemical tax-related cases, many courts did not make appropriate purposeful interpretations of the criminal law, and did not accurately determine the tax interests infringed upon by petrochemical tax-related cases, which led to a large number of such cases being convicted of the offence of fraudulently opening VAT special invoices. We are of the view that cases in the petrochemical industry that have been convicted of false invoicing have been incorrectly identified as facts and incorrectly applying the law, and that appeals can still be actively filed.

I. Analysis of the incriminating provisions of the judicial interpretations of the Supreme People's Court and the Supreme People's Procuratorate on the offence of false invoicing of VAT special-purpose goods

Paragraph 2 of Article 10 of the Judicial Interpretation of the Supreme People's Court and the Supreme People's Procuratorate stipulates that, "if the purpose of inflating the performance, financing or lending is not to fraudulently offset the tax, and if there is no fraudulent loss of tax due to the offsetting, the offence shall not be punished as this offence, and if it constitutes any other offence, the person shall be prosecuted for the criminal liability for the other offence in accordance with the law". This provision is an exculpatory provision, which gives the party concerned the opportunity to prove the offence and is of great significance. In the author's opinion, two conclusions can be drawn from the exculpatory clause:

(i) The legal interest protected by the offence of false VAT invoicing is VAT in the form of a credit against which the tax is levied.

The use of the expressions "fraudulent offset" and "fraudulent loss of tax due to offset" in the offence provision indicates that the offence of fraudulently opening VAT special invoices is mainly aimed at fraudulent offsetting, and that "offset" has a stable and clear meaning in tax collection and management. "Offsetting" has a stable and clear meaning in tax collection and management, and refers exclusively to the tax collection and management method of "input tax credit" adopted in the general method of value-added tax calculation.

Some opposing viewpoints point out that the concept of "offset" is not always used in VAT administration, for example, the concept of "approved deduction of input tax" also exists in the field of VAT on agricultural products, so the concept of "fraudulent offset" cannot be fully equated with VAT. Therefore, "fraudulent deduction" cannot be completely equated with VAT, and we believe that such understanding is contrary to the legislative intent of VAT. Approved deduction of VAT on agricultural products belongs to a special means of input tax deduction, and the concept of "approved deduction" is only adopted to differentiate from the levy and management method of input tax deduction of self-filled invoices for the purchase of agricultural products, and it is also clearly stipulated in the second article of the "Pilot Measures for Approved Deduction of Agricultural Products for Input Tax" that In Article 2 of the Pilot Measures for the Implementation of Approved Deduction of Input VAT on Agricultural Products, it is also clearly stipulated that "Pilot taxpayers who purchase agricultural products for offsetting input VAT shall be subject to these Measures", which is also sufficient to show that the approved deduction belongs to a special form of VAT input credit on agricultural products, and it is still a subordinate concept of VAT input credit, and is not a concept of the same level as that of input deduction.

Another opposing view is that the concept of "deduction" also exists in the fields of enterprise income tax and consumption tax, so that "fraudulent deduction" cannot be fully equated with value-added tax, and we believe that this understanding is also inappropriate. Firstly, Article 8 of the Enterprise Income Tax Law specifies that costs and expenses shall be deducted from the calculation of taxable income by way of "deduction", which is the concept of "pre-tax deduction" as we usually understand it. Although the State Administration of Taxation (SAT) Notice No. 81 of 2015 and other documents have adopted the expression of "deduction" of investment amount against taxable income, the deduction here still belongs to the subordinate concept of pre-tax deduction, which is a special form of pre-tax deduction, and does not mean that there is a "pre-tax deduction" in the calculation of taxable income for enterprise income tax. It does not mean that there are two ways of calculating the taxable income of enterprise income tax: "pre-tax deduction" and "credit". The "deduction" in the field of consumption tax mainly appears in Article 4(2) of the Provisional Regulations on Consumption Tax, which states that if the commissioned party uses the commissioned taxable consumer goods for the continuous production of taxable consumer goods, the tax paid shall be allowed to be deducted in accordance with the regulations, but the "deduction" in the field of consumption tax is not a special form of pre-tax deduction. However, "credit" here is not a rigorous concept of tax law, and does not constitute the so-called "consumption tax credit" system of levy and management, but only means that the continuous production of taxable consumer goods for taxable consumer goods can be "deducted", "deducted", "deducted", "deducted", "deducted", "deducted", or "deducted". It only means that the continuous production of dutiable consumer goods can "deduct" or "deduce" the consumption tax already paid. This can be supported by other consumption tax policies, for example, Cai Fa [2012] No. 8 stipulates that "if the commissioning party sells the recovered taxable consumer goods ...... at a price higher than the taxable price of the commissioning party ......, the commissioning party shall be allowed to deduct the consumption tax at the time of tax calculation". The concept of "deduction" is used in the provision that "the entrusted party shall be allowed to deduct the consumption tax that has been collected and paid on behalf of the entrusted party". In addition, Article 2 of the State Administration of Taxation Announcement No. 1 of 2018 provides that "if the gasoline, diesel oil, naphtha, fuel oil and lubricating oil recovered from outsourcing, importing and entrusted processing are used for the continuous production of dutiable finished products ......, the amount of consumption tax paid shall be deducted according to the provisions. "The concept of "deduction" is also used. Therefore, the "deduction" in the field of consumption tax is an unstable term that has not formed a unified concept, and obviously cannot be used as the basis for interpreting the concept of "fraudulent deduction" in the judicial interpretations of the Supreme People's Court and the Supreme People's Procuratorate, or as the basis for interpretation of the concept of "fraudulent deduction" in the judicial interpretations of the Supreme People's Court, The Supreme People's Procuratorate of the judicial interpretation of "fraudulent credit" by the object.

(ii) The commission of an act of false invoicing is not the same as the purpose and danger of "fraudulent deduction of VAT".

According to the legislative logic of the judicial interpretation of the Supreme People's Court and the Supreme People's Procuratorate, the first paragraph of Article 10 stipulates the offence of false VAT invoices, and the second paragraph stipulates the provision of the crime, which means that the first paragraph is the basis of the second paragraph, and only when the perpetrator has carried out the act of false invoicing does it need to be further analysed as to whether or not it has the purpose and dangerousness of "fraudulently obtaining the offsetting of the value-added tax". It means that the first paragraph is the basis of the second paragraph. It also means that there is no necessary connection between the act of false opening and "fraudulent deduction of VAT". In the author's view, the following cases are the main examples of those who commit the act of fraudulent opening but do not have the purpose and danger of "fraudulently obtaining VAT credit":

1. If the actor, as a general taxpayer, purchases VAT taxable items, pays a tax-inclusive price but does not obtain an invoice, and obtains a special VAT invoice from a third party, and the total amount of the price and tax does not exceed the purchase price paid by the actor. In this case, the perpetrator obtains the right of deduction in the procurement process, and chooses to issue invoices on behalf of the perpetrator because the right of deduction has not been fulfilled, because the tax deduction does not exceed the input tax amount borne by the perpetrator, and the main purpose of the perpetrator is to realise the right of deduction, rather than to "fraudulently obtain deduction" without the right of deduction, and the perpetrator's act of deduction is only limited to realisation of the right of deduction, and does not result in the loss of tax by fraud. The credit behaviour is limited to the realisation of the right to take credit and does not result in fraudulent loss of tax. It should be noted that only the purchaser (the invoiced party) meets the conditions for the offence. For the invoicing party, if it has the indirect intention of letting the invoiced party cheat the tax, it can still be regarded as having the purpose of helping other people to cheat the tax, and cannot certainly be convicted of the offence. For the seller, although it does not constitute the offence of false invoicing of VAT, if it fails to declare the tax at the time of sale, it should be investigated for the legal responsibility of tax evasion accordingly.

2. If the act of fraudulent invoicing is carried out but the tax credit function is not utilised. VAT is a tax levied on the value-added amount of taxable items, and there are two ways to realise the tax on value-added amount, one is to calculate VAT in accordance with the tax rate by subtracting the purchased amount of taxable items from the sales of taxable items, and the second is to calculate output tax in accordance with the tax rate by the sales of taxable items, and input tax in accordance with the tax rate by the purchased amount of taxable items, and then to calculate the tax payable amount by the difference, i.e., the deduction mode. Therefore, the ultimate goal of the credit model is to tax the value added, and it is designed for the correct calculation of the VAT payable. Using the invoice credit function to fraudulently offset VAT is able to encroach on national tax benefits on a large scale at a very small cost, which is a serious social hazard and should be punished as a felony, which is also the jurisprudential basis for setting a higher statutory penalty for the offence of false invoicing of VAT. However, with the development of the society, VAT invoices are endowed with other functions, such as financial accounting function, pre-tax deduction voucher function, and consumption tax deduction function for continuous production of taxable consumer goods, which have nothing to do with the input credit function. For those who have committed the act of false invoicing but have not made use of the deduction function to achieve the fraudulent deduction of VAT, they do not have the purpose and danger of "fraudulent deduction of VAT", and are not for the purpose of unlawfully appropriating the VAT interests of the State, so the social harm is far lower than that of the crime of false invoicing of VAT special purpose invoices.

II. Business model of tax-related cases in the petrochemical industry

The main product of the petrochemical industry is refined oil, which is a taxable consumer product subject to consumption tax, and the core purpose of tax-related cases in the petrochemical industry is to evade consumption tax. According to the Provisional Regulations on Consumption Tax, refining enterprises need to pay consumption tax in accordance with the law when they purchase non-taxable consumer products such as crude oil and process them into taxable consumer products such as fuel oil. As it is difficult for the tax authorities to monitor the production and processing of the refining enterprises in real time during the tax collection and management, the monitoring of the production behaviour has been transformed into the monitoring of the invoice name of the input and output items. If a refining enterprise obtains invoices for crude oil and issues invoices for fuel oil and other refined oil products, the tax authority considers that the refining enterprise has processed and produced, and should declare and pay consumption tax. While the refining enterprise purchases crude oil and obtains crude oil invoice, and still issues crude oil invoice for foreign sales of refined oil, or purchases crude oil and obtains refined oil invoice, and issues refined oil invoice for foreign sales of refined oil normally, it is reflected as trade behaviour on the books, and even if the processing and production behaviours have actually occurred, it is difficult for the tax authorities to effectively monitor the situation, so as to achieve the evasion of excise tax payment obligations.

(i) Traditional tax-related cases in the petrochemical industry

Traditional tax-related cases are mainly manifested in the form of variable bill cases, with the following two main types of variable bill patterns:

1, used in the field of production of false consumption tax change ticket, the core of this change ticket mode is the refining enterprise to change the invoice name of the raw material procurement process, that is, the procurement of crude oil, crude oil invoices, through the change of the invoice enterprise to change the invoice name to refined oil, and then refined oil invoices back to the same time, while the production of crude oil cargoes into refined oil, the normal sales to the outside world, forging the procurement of refined oil, the sales of refined oil of the pure trade business.

2. The change of invoice for circulation mainly refers to the refining and chemical enterprises producing refined oil products and selling them to the outside world, still issuing invoices for crude oil or chemical products to avoid tax obligations, and then changing the invoice name to refined oil products through the change of invoice enterprises to cooperate with the downward circulation of refined oil products goods.

(ii) New tax-related cases in the petrochemical industry

In order to fundamentally prevent the petrochemical trading enterprises from changing their invoices, the State Administration of Taxation (SAT) issued the Announcement on Relevant Issues Concerning the Collection and Management of Consumption Tax on Refined Products (SAT Announcement No. 1 of 2018) in January 2018, and formally went online with the Refined Products Oil Invoice Module system in March 2018. The refined oil product invoice module imposes significant restrictions and norms on the use of refined oil product invoices by trading enterprises and production enterprises. However, the fundamental problem of monopoly in the refined oil market will remain for a long time, and the cost-cutting needs of refining and chemical enterprises will always exist, based on which the invoice offences in the petrochemical industry will not go away, and new modes of changing invoices have emerged.

There are various new modes of invoicing in practice, such as using historical false inventory for external invoicing, forging customs import payment letters for refined oil to falsely increase inventory for invoicing, relying on a production enterprise to invoice for tax arrears, outsourcing processing for tax arrears for invoicing, using the time difference between the red punch of the invoices of refined oil to invoice for external invoicing, tampering with the system by using hacker technology to violently invoicing, and obtaining invoices on behalf of the retailers of refined oil products such as petrol stations, and other modes of invoicing. However, the core purpose of these cases is still to evade consumption tax.

III. Legal analysis of tax-related cases in the petrochemical industry

Combined with the provisions of the judicial interpretations of the Supreme People's Court and the Supreme People's Procuratorate, the legal interests infringed by tax-related cases in the petrochemical industry are fundamentally different from those of the general offence of fraudulent invoicing, and acts in the petrochemical industry that are aimed at evasion of excise tax, do not have the purpose of fraudulently offsetting value-added tax, and do not create the danger of value-added tax loss should be excluded from the offence of fraudulently issuing special invoices for value-added tax. Specifically:

(i) Petrochemical invoicing is motivated by excise tax evasion and infringement of national excise tax interests

For the purpose of consumption tax evasion, refining and chemical enterprises, while actually using crude oil to process and produce finished oil products such as fuel oil, transfer the change of invoice name to the upstream or downstream enterprises in the purchasing and selling chain, or when purchasing raw materials for non-taxable consumer goods, request the suppliers to issue (or the third-party enterprises to issue on behalf of them) invoices with the name of taxable consumer goods, so as to illegally make consumption tax deductions, and take advantage of the loopholes of the taxation levy and management to They take advantage of the loopholes in tax collection and management to circumvent the consumption tax obligations they should have borne. All these behaviours are in line with the purpose of consumption tax evasion and infringe upon the interests of national consumption tax.

(ii) The petrochemical alteration of the invoice has no purpose of fraudulently offsetting VAT and there is no risk of fraudulently offsetting VAT benefits

In practice, tax-related cases in the petrochemical industry, in addition to the participation of refining and chemical enterprises and ticket-changing enterprises, usually lengthen the transaction chain and design multiple over-invoicing links in order to make the behaviour more covert. However, no matter how many over-invoicing links are added, each transaction subject in the chain issues invoices in accordance with the actual quantities and amounts of oil products, confirms the amount of output tax according to the amount of tax recorded in the actual invoices issued and confirms the amount of Input tax is recognised according to the tax amount recorded in the actual invoices issued, and input tax is recognised according to the tax amount recorded in the actual invoices obtained. The VAT rates of crude oil, chemical raw materials and refined oil products are the same, and the change of product name does not affect the VAT obligation. The act of changing invoices does not have the subjective purpose and objective danger of cheating VAT, and has no possibility of infringing on the VAT interests of the State.

To sum up, the criminal act combated by the offence of false invoicing is the act of using VAT invoices to cheat the state tax, and the core is "cheating"; the criminal act combated by the offence of tax evasion is the act of maliciously evading the tax obligation through various means, and the core is "evasion". If the act of petrochemical alteration of invoices only makes use of the function of the invoices to make false consumption tax declaration and evades the payment of consumption tax, does not cause the loss of national value-added tax, and does not violate the protection of the legal interests of the crime of false VAT invoices, it is not appropriate to determine that it constitutes the crime of false VAT invoices. The judicial authorities cannot arbitrarily overstep the boundary between the two offences on the basis of the amount of tax loss, especially the offence of false VAT invoicing cannot be arbitrarily expanded. Otherwise, it will be a serious violation of the basic principle of the criminal law of the appropriateness of crime and punishment, and a serious violation of the fairness and justice of the criminal law.

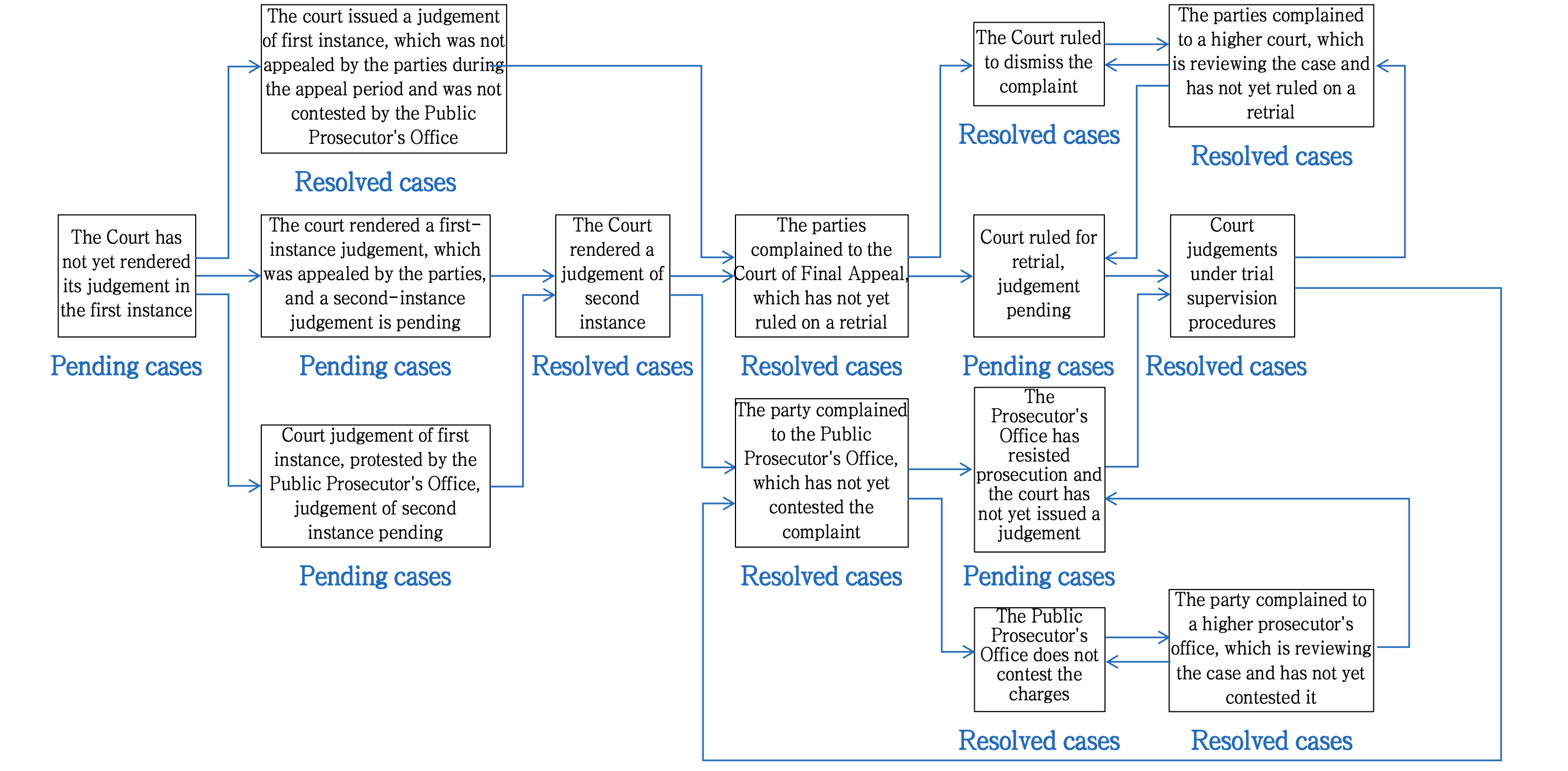

IV. Analysis of the temporal validity of the judicial interpretations of the Supreme People's Court and the Supreme People's Procuratorate

(i) Judicial interpretations by the Supreme People's Court and the Supreme People's Procuratorate as a reduction of the intent of the criminal law

According to the principle of legality of offences and penalties, the basic issues of incrimination and punishment, such as the elements of the offence and the provisions of the offence, can only be regulated by the criminal law. Judicial interpretation can only explain the criminal law, clarify the legal application of the criminal law, but can not go beyond the criminal law to set up a separate offence, incriminating provisions. Therefore, the Supreme People's Court, the Supreme People's Procuratorate judicial interpretation of the "fraudulent tax deductions" is not a new legal provisions, but the criminal law of the intent of the restoration. The determination of crime and non-crime is stable, and it is not possible to conclude that an act constitutes a crime before the Supreme People's Court and the Supreme People's Procuratorate Judicial Interpretations were issued, but rather it should be assumed that before and after the issuance of the Judicial Interpretations of the Supreme People's Court and the Supreme People's Procuratorate, the conclusion of whether or not the act is incriminated is the same, and that the absence of provisions in the Criminal Law and the Judicial Interpretations of the past belongs to the technical problems of the legislation.

Therefore, for petrochemical tax-related cases heard before the implementation of the judicial interpretations of the Supreme People's Court and the Supreme People's Procuratorate, the judicial organs should adopt the principle of purposeful interpretation and revert to the criterion of guilt that was omitted from the Criminal Law and the old judicial interpretations, i.e., the offence of fraudulent issuance of value-added tax invoices shall not be constituted if the offence is not committed with the purpose of fraudulently offsetting the tax and if no tax is fraudulently lost due to the offsetting. If the judicial authorities have not determined the loss of value-added tax and have not considered the criteria for the offence before sentencing the person to constitute the offence of fraudulent issuance of value-added tax invoices, it is obvious that it is an error in the determination of the facts and an error in the application of the law.

(ii) Judicial interpretations of the Supreme People's Court and the Supreme People's Procuratorate apply to all decided and pending petrochemical tax-related cases

The judicial interpretations of the Supreme People's Court and the Supreme People's Procuratorate have been in force since 20 March 2024, and in accordance with the relevant provisions of the Criminal Procedure Law and the Provisions of the Supreme People's Court and the Supreme People's Procuratorate on the Application of the Temporal Effectiveness of the Judicial Interpretations of Criminal Laws (No. 5 of the Interpretation of Higher Procuratorate [2001]), the temporal effectiveness of the judicial interpretations of the Supreme People's Court and the Supreme People's Procuratorate is distinguished from the judgement of the four situations:

1. If the offence was committed after 20 March 2024, the new judicial interpretation shall apply as a matter of course.

2. If a criminal act was committed before 20 March 2024 but was a pending case when the judicial interpretations of the Supreme People's Court and the Supreme People's Procuratorate came into effect, in principle, the provisions of the old law shall be applied to deal with the case, but if the judicial interpretations of the Supreme People's Court or the Supreme People's Procuratorate are more favourable to the parties concerned, they shall be applied to deal with the case as provided for by the judicial interpretations of the Supreme People's Court and the Supreme People's Procuratorate.

3. If the offence was committed before 20 March 2024 and was a res judicata case when the judicial interpretation of the Supreme People's Court and the Supreme People's Procuratorate came into effect, no further changes will be made if the facts are found to be correct and the applicable law is correct in accordance with the provisions of the old law.

4. If a criminal act occurred before 20 March 2024 and was a decided case when the judicial interpretation of the Supreme People's Court and the Supreme People's Procuratorate came into force, the trial supervision procedure shall be initiated if the facts are found to be incorrect and the law applied in accordance with the provisions of the old law.

Therefore, for pending petrochemical tax-related cases, the provisions of the judicial interpretations of the Supreme People's Court and the Supreme People's Procuratorate are certainly applicable, and the application of the exculpatory provisions can be actively advocated. For pending petrochemical tax-related cases, if the court trial does not take into account whether the party concerned has the purpose of fraudulently offsetting the value-added tax, or whether it has caused fraudulent loss of the value-added tax and imposes a judgement that constitutes the crime of fraudulently issuing value-added tax special invoices, the Supreme People's Court should be applied, The legislative intent of the criminal law as clarified in the judicial interpretation of the Supreme People's Procuratorate shall be applied to initiate trial supervision procedures.

V. Recommendations: active appeals in cases of false convictions for excise tax evasion in the petrochemical industry

Tax-related criminal proceedings are one of the more specialised and delicate areas of criminal proceedings, and petrochemical invoicing cases are particularly difficult. In practice, if a proper defence strategy cannot be formed to accurately explain the motive, subjective purpose and social harm of the petrochemical vote-changing case, it will be difficult to guide the judicial authorities to examine the facts of the case that will affect the conviction and sentence, which will lead to the judge to make a deviation from the just sentence based on the established erroneous cognition. The defence strategy for the petrochemical vote-changing case should focus on the following three points:

1. Status of the VAT chain

Firstly, it is necessary to examine whether the invoicing parties in the chain have paid the full amount of tax on the invoices issued, and whether the tax deduction of the invoices obtained by the invoiced party is limited to the output tax generated by the invoices issued externally in this business. If the invoicing party does not pay the VAT accordingly, there is the problem of tax evasion and the legal responsibility for tax evasion needs to be pursued. If the invoiced party obtains invoices not only for offsetting the invoices issued externally in the business, but also for offsetting the output tax generated by other businesses, there is the behaviour of obtaining false invoices and the legal responsibility for false invoicing needs to be pursued.

2. Principles of excise duty losses

The subjective purpose of the petrochemical cheque-changing actors and the objective result of their behaviour are both consumption tax evasion. Moreover, the enterprise that committed the act of changing the cheque only obtained the benefit of changing the cheque fee, and the refining enterprise was the biggest beneficiary in the whole chain, and the income of the whole chain also came from the excise tax evaded by the refining enterprise.

3. Legal application of the offences of false VAT invoicing and tax evasion

After clarifying the principle of consumption tax loss, it should further combine the two constituent elements that the offence of false VAT invoicing actually requires the intent to fraudulently offset the value-added tax and the result of causing the national value-added tax loss, and argue that petrochemical alteration of invoices does not constitute the offence of false VAT invoicing and belongs to the act of evading tax. At the same time, it actively advocates the application of administrative pre-procedures to avoid criminal penalties through the payment of back taxes and late fees and the payment of fines.