The 2024 Annual Work Conferences of Procuratorates and Courts deployed to deepen the reform of compliance of enterprises involved in cases, and the road to compliance in tax-related cases should be ta

I. The 2024 National Conference of Chief Procurator was held: Deepen the reform of compliance of enterprises involved in cases, and deploy the "Procuratorate Protects Enterprises" action

On January 14, 2024, the National Conference of Chief Procurator was held in Beijing, which comprehensively summarized the procuratorial work in 2023 and deployed the main tasks for 2024. The meeting emphasized that in the new year, the procuratorial work should focus on the construction of a law-based business environment, adhere to the equal protection of all types of business entities in accordance with the law, deepen the reform of compliance of enterprises involved in cases, and deploy and carry out the special action of "Procuratorate Protects Enterprises".

The 2024 "Procuratorate Protects Enterprises" special action emphasizes that procuratorial department should "accurately grasp the boundaries between crimes and non-crimes in intersecting criminal and civil cases in accordance with the law, and strengthen supervision over the use of criminal means to meddle in civil and economic disputes". It is necessary to "continuously protect the property rights of enterprises and the rights and interests of entrepreneurs, optimize the environment for the development of private enterprises", and further implement the policy of protecting and promoting the development and growth of the private economy.

The meeting emphasized that in 2024, it is necessary to deepen the reform of compliance of enterprises involved in cases. Procuratorial departments should play a leading role, improve third-party oversight and assessment mechanisms, handle more high-quality and efficient cases that demonstrate the system value, and have leading significance, promote the application of compliance in criminal proceedings such as prosecution and trial, and jointly establish a modern judicial system with Chinese characteristics for enterprises compliance."

II. The 2024 National Conference of Chief Justices of High Courts was held: Promote the development and growth of the private economy, and advance the reform of compliance of enterprises involved in cases

On January 14, 2024, the National Conference of Presidents of High Courts was held in Beijing to summarize the work of the courts in 2023 and study the main tasks in 2024. The meeting emphasized that in 2024, it is necessary to continue to optimize the legal environment for the development and growth of the private economy, and "take the promotion of reform of compliance of enterprises involved in cases as an important starting point for implementing both crime and governance and promoting the healthy development of corporate compliance operations", and courts at all levels should sincerely achieve both "strict management" and "care".

As an important measure of the court's "strict management and care", the reform of compliance of enterprises involved in cases has made comprehensive arrangements as early as September 2023 at the National Conference on the Promotion of the Reform of Compliance with Laws and Regulations of Enterprises Involved in Cases. The promotion committee proposed that carrying out the compliance reform of enterprises involved in cases is a new task of the courts, and that "courts at all levels should work together to build an enterprise compliance system and governance system with Chinese characteristics", pointing out the direction and path of the compliance reform of enterprises involved in cases in the trial stage.

III. 2023 Tax-related Regulatory Trends and Case Review: The tax-related criminal risk continues to rise, and the entity private enterprise is rescued under strict management

Both the Supreme People's Procuratorate and the Supreme People's Court have proposed: love should be combined with strict management. As a concentrated embodiment of "benevolence", the compliance reform of the enterprises involved in the case is precisely the result of "strict management": that is, on the premise of severely cracking down on corporate crimes, saving the enterprises and entrepreneurs with good business conditions and development prospects and contributing to economic development is the work of making up for the outbreak of criminal offenses.

Judging from the form of tax-related supervision in 2023, the criminal risks faced by enterprises such as false opening and tax fraud will continue to rise in 2024. In July 2023, the State Administration of Taxation, the Supreme People's Procuratorate, the Supreme People's Court, and other seven departments held a meeting to promote the joint crackdown on tax-related violations and crimes, summarizing the effectiveness of the normalized crackdown on false tax fraud and deploying the next stage of work. The Supreme People's Procuratoratejoined the joint crackdown mechanism in October 2021 and played an important role.

From October 2021 to the end of May 2023, the joint crackdown mechanism has inspected a total of 270,000 enterprises suspected of fraudulent tax issuance, identified 10.4815 million false invoices, and recovered 11.78 billion yuan in export tax rebate losses. As a result, many private entities are involved in criminal cases of false issuance and tax fraud, and the enterprises are facing bankruptcy and entrepreneurs are at risk of being detained, and they urgently need to be rescued by the compliance mechanism.

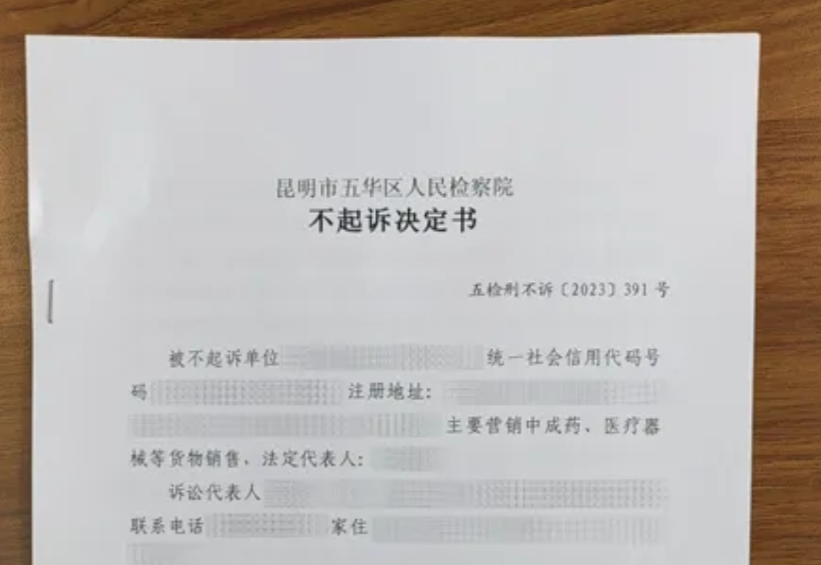

In September 2023, a pharmaceutical company in Yunnan received a non-prosecution decision from the Wuhua District Procuratorate of Kunming City. The company is a pharmaceutical company that has been operating continuously for more than 30 years, but due to the false issuance of special VAT invoices, it was transferred to the procuratorate by the public security for review and prosecution, and the relevant responsible persons face criminal liability. After the case was discovered, the company actively paid back taxes and fines, carried out compliance rectification under the leadership of the procuratorate, and obtained a decision not to prosecute.

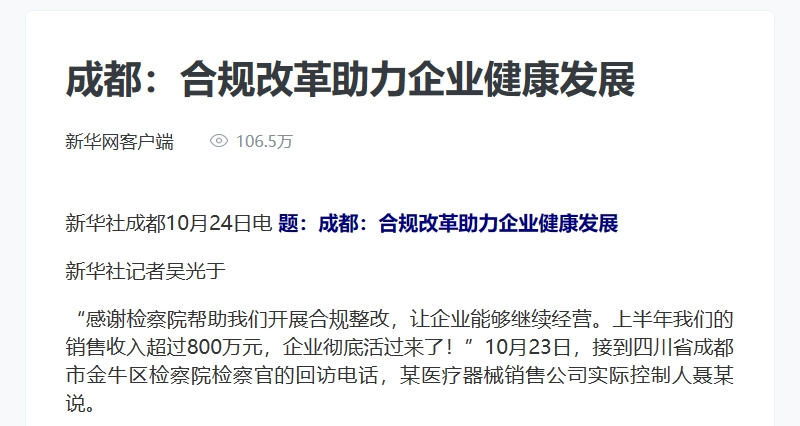

In October 2023, a medical device sales company located in Chengdu accepted a return visit from the Chengdu Jinniu District Procuratorate on the company's compliance rectification. During the period from 2014 to 2020, the company accepted false VAT invoices, and the tax deduction was as high as more than 290 yuan, and the responsible person faced criminal liability of more than 10 years in prison. In order to save the entity, the procuratorate carried out compliance rectification with the approval of the superiors. In November 2022, the company's rectification and acceptance were completed, and the procuratorate made a sentencing recommendation of "probation" for the actual controller of the enterprise. In the subsequent trial, the court recognized the results of the rectification and sentenced the actual controller of the enterprise to a suspended sentence.

There has also been a breakthrough in compliance reform at the trial stage. OnApril 27, 2023, the Intermediate People's Court of Wuhu City, Anhui Province, pronounced a second-instance verdict on a case of false issuance of special VAT invoices, and the defendant Xing X committed the crime of falsely issuing special VAT invoices and was sentenced to be exempted from criminal punishment. This is the first case in the country in which the compliance rectification of an enterprise was applied in the second instance. During the trial, the court held that the enterprise and entrepreneur had a good attitude in admitting guilt after the case, actively paid back taxes and fines, voluntarily pleaded guilty and accepted punishment, and had a strong sense of voluntary rectification, which met the conditions for compliance rectification of enterprises. After acceptance by the third-party supervision and assessment team, a judgment was made to exempt him from criminal punishment.

Overall, in 2024, the policy orientation of "strict management" and then "love" will still be implemented, and seven departments, including the Supreme People's Procuratorate and the Supreme People's Court, will continue to crack down on tax-related illegal and criminal activities, and at the same time save entity private enterprises through compliance rectification.

IV. What should I do if the tax-related criminal risk has erupted? 2024 Compliance Reform Direction: Deepen the protection of entities

Since 2023, under the joint crackdown of seven departments, many entity private enterprises have been sentenced to criminal penalties on suspicion of false issuance and tax fraud. After the outbreak of the case, the business of the originally well-run enterprise stalled, and the relevant person in charge was detained, and there was no remorse.

For these enterprises and entrepreneurs who are in line with the spirit of the central government's "six stability and six guarantees", they can pay back taxes, recover economic losses through the mechanism of compliance rectification, and carry out the construction of the internal tax compliance system with the help of tax professional lawyers, so as to achieve the best result of non-prosecution or reduction of criminal punishment.

Moreover, judging from the arrangements of the 2024 work deployment meetings of the two supremes, the compliance reform of the enterprises involved in the case will be further deepened, which will be more conducive to the protection of enterprises and entrepreneurs. By summarizing the current pain points and problems of the criminal compliance system, we believe that the reform direction in 2024 will mainly focus on the following aspects:

First, the compliance system of the enterprise involved in the case has been statutorized. The compliance reform of the enterprises involved in the case has achieved good results in practice. However, this system has not yet been incorporated into the Criminal Procedure Law, and corporate compliance rectification can only be considered as a discretionary sentencing circumstance, which is not conducive to effectively playing the function of criminal compliance. With the deepening of the reform, this system will be statutory, and the results of corporate compliance rectification will also be regarded as a statutory mitigating circumstance, laying a legal foundation for the enterprises and entrepreneurs involved in the case to obtain judicial treatment such as non-prosecution and exemption from criminal punishment.

Second, remove the restrictions on the activation of the compliance mechanism of the enterprises involved in the case. In practice, some local internal regulations prohibit compliance rectification in serious crime cases that may be sentenced to more than 10 years, but this provision is unreasonable and illegal. On the one hand, the relevant provisions of the Supreme People's Procuratorate and the Supreme People's Court on the compliance of enterprises involved in cases do not impose restrictions on the length of sentences in cases; on the other hand, in practice, some large-scale entity production enterprises and groups, such as steel, coal, and petrochemical enterprises, can easily exceed the threshold of 2.05 million yuan in taxes due to their good economic returns and high turnover. If these large enterprises and large groups that have made outstanding contributions to the local economy, taxation, and employment are not complied with, resulting in their closure and bankruptcy, it is not in line with the purpose of the compliance reform of the enterprises involved in the case. Therefore, with the deepening and normalization of compliance reform, the restrictions on places where felonies must not comply with regulations have been abolished.

Third, compliance rectification is extended to the trial stage. As the court participates in the compliance reform of the enterprises involved in the case, there will be more opportunities for the private enterprises and entrepreneurs involved in the case to comply with the law. On the one hand, due to the longer trial period, the time given to the enterprise to pay taxes and late fees can also ensure that the enterprise can carry out compliance in a solid manner; on the other hand, if the enterprise does not file a compliance application during the review and prosecution process of the procuratorate, it can now file a compliance application in the trial stage or even the second-instance trial stage, so as to provide more adequate protection measures for the entity enterprise.

Fourth, private entrepreneurs are the most valuable wealth of private enterprises, and the reform will intensify the protection of entrepreneurs. In the past, some case-handling organs held the viewpoint of "letting the enterprise go and severely punishing the responsible", ignoring the major and even decisive influence of private entrepreneurs on the development of enterprises. At present, most of China's private enterprises belong to family enterprises, and the business development decision-making of enterprises, customer liaison and maintenance, and employee recruitment and selection all rely on the main person in charge of the enterprise. Therefore, in many tax-related criminal cases, once the person in charge of the enterprise is detained, the enterprise quickly stops work and production, and cannot continue to operate. This is also the reason for the criminal policy of "fewer detentions, cautious prosecution and cautious arrest". Therefore, the protection of private enterprises is first and foremost to protect private entrepreneurs, and the compliance rectification of enterprises should not only be for enterprises, but also for entrepreneurs.

From the above reform directions, it can be seen that the compliance rectification system for enterprises involved in cases in 2024 will still give enterprises and entrepreneurs in tax-related criminal cases a chance to turn over a new leaf. Private enterprises and entrepreneurs should take the initiative to pay attention to their tax compliance and criminal compliance systems, and improve their ability and level to respond to and resolve tax-related criminal risks.

V. The road to corporate tax compliance: Actively seek professional tax forces to assist in compliance construction

For private enterprises, 2024 is a year in which tax-related supervision will continue to be stricter. Tax collection and management reforms such as "tax governance by numbers" and tax big data have been deepened, and corporate tax risks have continued to erupt, showing the characteristics of typology, industry, and concurrent administrative and criminal liability. In order to prevent and respond to tax risks, enterprises should raise their awareness of tax law compliance and establish an effective tax compliance management system in the process of enterprise establishment and operation, so as to avoid legal sanctions, financial losses, reputational damage and even criminal liability that may be suffered by failure to comply with tax laws. Specifically, private enterprises need to continue to build a compliance mechanism from the following aspects:

First of all, it is necessary to carry out regular tax health checks, and professional tax professionals will conduct tax investigations on the business model, financial and tax systems of the enterprise, investigate, identify and analyze major tax risk points, guide the enterprise to carry out tax compliance rectification, and sort out and improve the business process. At the same time, through the promotion of tax policies, the culture of tax compliance is cultivated.

Second, we must continue to build a tax compliance management system. Under the guidance of professional tax law forces, enterprises should assist enterprises in establishing tax compliance systems and organizational structures, and establish well-functioning tax risk identification, assessment, risk control and response mechanisms, as well as risk control and response mechanisms, taking into account their own business conditions, tax risk characteristics and existing internal risk control systems.

When criminal risks erupt, private enterprises should also resolve and respond to relevant risks through criminal compliance rectification. Criminal compliance is particularly different from the daily compliance of enterprises in that third-party assessment agencies focus on the prevention and response of enterprises to the outbreak of risks, so as to ensure that enterprises will not commit relevant tax-related violations and crimes in the future, so it is particularly necessary to efficiently and accurately identify internal and external tax risks and put forward effective prevention and disposal suggestions during the limited compliance period.

At the same time, the enterprise should be counseled to conduct criminal compliance rectification counseling, set up a compliance rectification working group, analyze the causes of violations and crimes, formulate a targeted compliance rectification plan, and issue a targeted compliance rectification planThe compliance plan and compliance rectification report assist the enterprise to accept the inspection and evaluation of the judicial authorities and third-party organizations, and help the enterprise successfully pass the acceptance of compliance rectification.